You will get a negative entry at SCHUFA faster than you might think.

Even if you have always paid your bills on time, repaid installments conscientiously and never overdrawn your credit line, it can happen that your so-called SCHUFA credit score suffers from a negative entry.

In fact, according to various studies, about one in three SCHUFA reports is incorrect.

Since hardly any company, bank or landlord wants to have a contractual partner who merely has a low credit rating, a bad SCHUFA report can have far-reaching consequences for your private and business life.

For this reason, today we will go into more detail about how the SCHUFA score comes about, what consequences a negative score has for you and what measures you can take to improve your improve your creditworthiness.

What is SCHUFA?

In fact, many people assume that SCHUFA is a government agency or a joint organization of German banks.

However, SCHUFA is a normal German private company that collects and stores creditworthiness data about German companies and individuals.

This creditworthiness data includes all information that provides indications of your payment history and creditworthiness, for example, whether bills and installments have been paid on time or credit relationships exist.

Due to its non-transparent evaluation processes, massive data storage and hundreds of thousands of false entries, SCHUFA has been criticized by data protection experts and consumer protection groups for years.

Some are even calling for a ban on the Schutzgemeinschaft für allgemeine Kreditsicherung, as SCHUFA is actually called.

At present, however, it does not look as if SCHUFA will disappear from the business world in the near future.

On the contrary, the importance of SCHUFA and the trust placed in the credit agency by companies and credit institutions has been increasing for years.

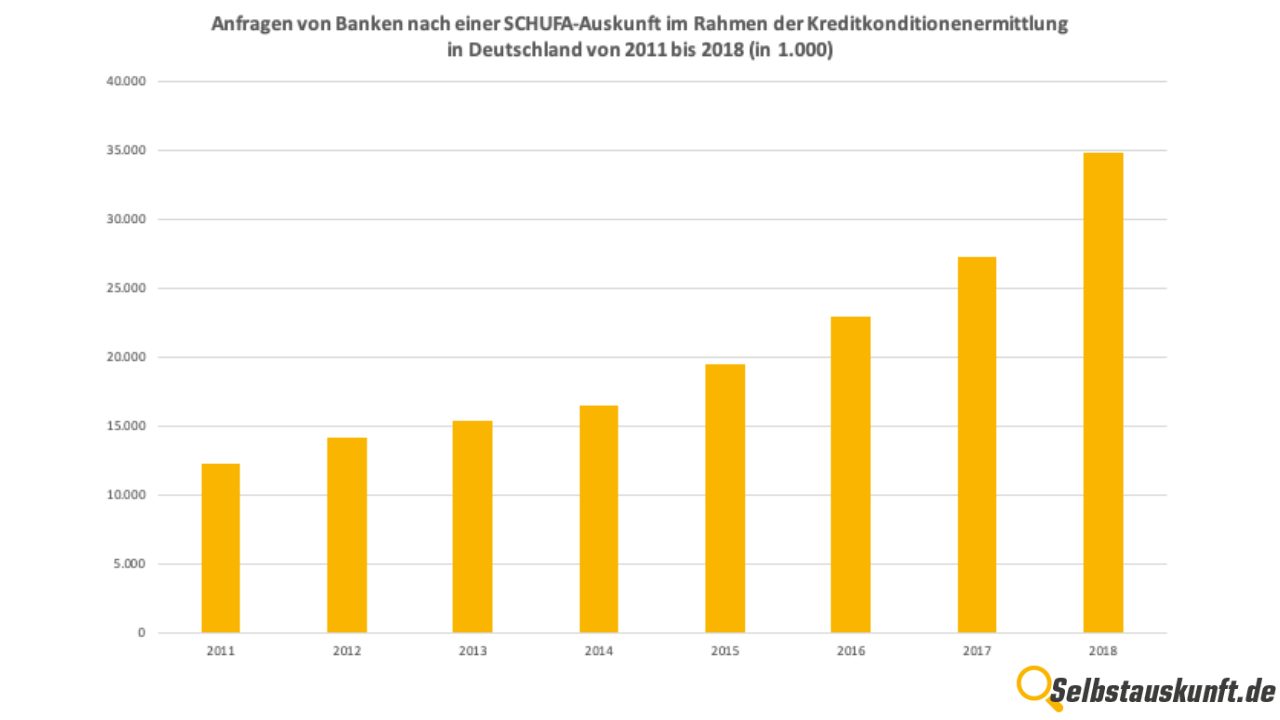

In the last 9 years, for example, the number of requests from banks has tripled.

This chart illustrates the number of requests for SCHUFA information from banks in the context of determining credit terms between 2011 and 2018.

In 2018, banks submitted a total of around 35 million inquiries to SCHUFA.

Consequently, you inevitably have to deal with your own credit rating - even if you don't approve of SCHUFA's business practices.

If you are well informed and know how the SCHUFA score is calculated, you can also take steps to improve your credit score.

What is the SCHUFA Score?

The SCHUFA score is a percentage value that can be used to classify the creditworthiness of individuals and companies.

This value indicates how likely it is that the customer will meet his payment obligations and forms the core of SCHUFA's credit rating.

The score thus enables contractual partners to quickly determine how high or low the customer's or tenant's risk of non-payment is.

The value scale goes from 1 to 100; the higher the value, the better the credit rating and the lower the risk of default.

100 can never be achieved, as a certain, unforeseeable residual risk can never be ruled out - for example, due to the sudden death of the payer.

The following list gives a good overview of how the individual percentage values are interpreted:

97.5% - 99.9% - very low risk of default

95.0% - 97.5% - low to manageable risk of default

90.0% - 95.0% - satisfactory to increased risk of default

80.0% - 90.0% - significantly increased to high risk of default

50.0% - 80.0% - very high default risk

below 50.0% - very critical default risk

Already from a score below 95% one should ask oneself directly: "How can I improve my credit rating?"

How does the SCHUFA score come about?

The bad news first: How exactly the score that SCHUFA uses to classify your creditworthiness is calculated is secret.

SCHUFA justifies its lack of transparency by stating that the scoring procedure represents the core of its business model and that this must be protected by secrecy.

In fact, the Federal Court of Justice ruled in 2014 that the SCHUFAthat SCHUFA does not have to disclose the method used to calculate the score.

However, it is obliged to provide all citizens with regular access to the SCHUFA data stored.

You can therefore request your request your personal SCHUFA self-disclosure (also online)check your creditworthiness and have any false entries removed.

This is, for example, one of the various measures that improve the creditworthiness can.

But back to the calculation of the SCHUFA score.

Although the exact method of calculating the credit score is not public, it is nevertheless known what data SCHUFA stores and basis is used to calculate the credit score:

Personal data

Of course, your score is not arbitrarily determined based on your last name or date of birth.

However, personal data such as your first & last name, place & date of birth, address(es) and gender also form an important basis for your score.

Finally, all data that is stored must be able to be assigned to a single person without any doubt.

Since many people have the same name, the other personal information is also used for the purpose of establishing identity.

Example: If Michael Mustermann from Munich lives in luxury, does not pay bills and one debt collection procedure after the next is opened against him, Michael Mustermann from Berlin should not have to answer for it just because they have the same name.

Bank, credit and account information

One of the most important data sources for SCHUFA is your bank and account information.

Although SCHUFA has no insight into your account movements, i.e. deposits and withdrawals, it does collect information on how many accounts you have, which and how many credit relationships exist and how many credit cards you have.

Every time you open a bank account (e.g. a current account) or apply for a loan, the bank forwards this information to SCHUFA.

It is suspected that opening too many bank accounts as well as using multiple credit cards has a negative impact on the SCHUFA rating.

In addition, your SCHUFA score suffers if you have a bank account, a loan or your credit card is canceled, because banks also transmit this data to SCHUFA, which is then stored there.

Do you want to improve your improve your credit ratingyou should therefore not keep too many bank accounts - but more on that later.

Contractual relationships and guarantees

In addition to banking information, SCHUFA also records what other long-term contractual relationships exist with you.

These include, for example, leasing, mobile communications or Internet contracts and other installment agreements.

The duration of the contractual relationship, whether payments have been received as agreed and information on any conduct in breach of contract are noted here.

In addition, your SCHUFA report will show whether you have provided guarantees, for example for a friend's loan.

Other negative features

If you are (or have been) involved in debt collection proceedings, have filed for personal insolvency or are entered in a debtors' register, this will also appear in your SCHUFA information.

How long this information is stored varies.

If you would like to find out more about this, please read our Article "SCHUFA entry: how long does it remain?".

There we go into detail about the SCHUFA deletion periods.

Positive features

When you consider how much data SCHUFA collects, you can quickly get a bad feeling.

However, you should know that SCHUFA also notes if you diligently meet your payments.

There are positive entries as well as negative ones.

In fact - according to SCHUFA - there is only positive information on over 90% of the persons deposited.

So if you are conscientious about meeting your payment obligations, you should not have a bad SCHUFA score.

However, it is important to order SCHUFA self-disclosure regularly to order and check and check it regularly in order to be able to quickly counteract negative or incorrect entries.

Negative SCHUFA score - what are the consequences?

If they do not have to deal acutely with their SCHUFA information, many people are quite uninterested in how their SCHUFA information and their credit score stand.

However, this is a big mistake, because one's circumstances can change at any time.

If you suddenly need a loan, are unexpectedly in need of financing, or are unexpectedly forced to look for a new place to live, you won't get far with a bad SCHUFA score.

Therefore, you should take early action that will improve your improve your credit rating.

All of these things are made more difficult or even impossible in some cases by a bad SCHUFA score:

Apartment search

Although no apartment applicant is legally required to provide the landlord with a SCHUFA report, proof of creditworthiness is expected in most cases.

Whether or not you comply is usually irrelevant to the landlord: normally, there are plenty of other competitors who are more than willing to do so.

The consequence: especially in large cities, you are quite likely to be excluded from the application process if you cannot or do not want to provide information.

After all, the landlord will then probably choose another candidate who can prove his creditworthiness.

Funding

Whether construction financing, car financing or financing for other projects and purchases: with a bad SCHUFA score, you usually either get no financing offers at all or, if you do, then only with immensely high interest payments.

Borrowing

When taking out a loan, the situation is similar to that of financing.

With a poor credit rating, hardly any bank will approve you for a loan, and if they do, then only with extraordinarily high repayment interest.

Account opening

Even opening ordinary bank accounts is anything but a piece of cake if your own credit score is insufficient.

Since checking accounts often have an overdraft limit and the bank must fear that you will overdraw it without the possibility of repayment, account opening requests are usually rejected as a precaution.

The only option you have in such a case is to open a prepaid checking account.

With these, however, one is often inflexible, which is why it pays to improve the SCHUFA to improve. Tricks and tips that will help you do this, we will cover in the further course.

Application for credit cards

Applying for credit cards is also difficult if your score is not good enough from the bank's point of view.

Since the bank theoretically pays in advance for credit card customers, it must be certain that the customers will be able to settle this amount on the due date.

If you have been reported to SCHUFA for poor payment history on several occasions in the past, it is rather unusual for a credit card application to be approved.

Increase in the payment limit or overdraft facility for the credit or debit card

Similar to credit card applications, the SCHUFA score is usually closely scrutinized when applying for an increase in the credit card limit or overdraft facility.

If the rating is poor, the bank will not approve you for higher payment limits.

Installment agreement

A new TV, a new couch or a new laptop: all these things cost a lot of money.

For this reason, many retailers now offer their customers installment financing.

Instead of having to have €1,200 ready right away, you can pay for your new smartphone in 24 months of €50 each, for example - provided your SCHUFA score is good enough.

This is because when you apply for installment payments, the merchants check carefully whether you are at risk of default.

If this is the case, you will not normally be offered an installment option.

Pay on account

Even if you want to pay on account, as is often the case especially with online shopping, a credit check is performed before the purchase is completed.

If your score is not sufficiently high, this form of payment will not be eligible for you.

Car Leasing & Car Financing

Leasing or financing a car will also not be possible if your credit score indicates poor payment history.

Of course, the business is only profitable for the financing provider if the customer also pays the installments on time and in full.

If you have a history of late payments, you will usually be excluded from such offers as a contractual partner.

Conclusion or change of cell phone or DSL contracts

Most people think directly of apartment hunting or credit applications when they hear the word "SCHUFA".

In fact, however, your SCHUFA is also checked for all kinds of contracts that require monthly payments.

This also includes cell phone and DSL contracts.

So, for example, if you want to change your outdated and overpriced cell phone contract or want a new DSL contract with faster Internet, it looks bad with a low credit score.

How can I improve my credit rating?

Now that it has become clear how important a clean SCHUFA is at all times (!), you are probably asking yourself a question:

How can I improve my SCHUFA?

That's why we'd now like to show you a few ways you can spruce up your credit score.

One thing in advance: There are some tricks that can improve the SCHUFA improve. Tricks or "hacks" do not exist here in the classic sense, however, and attempting to falsify or manipulate one's own SCHUFA information can have serious legal consequences.

For this reason, we expressly advise against attempts at deception!

But now for the legitimate tips:

1) Order the SCHUFA self-disclosure on a regular basis

Only if you have a constant overview of your SCHUFA entries - whether positive or negative - can you ensure that your SCHUFA score remains in the green.

In the meantime, you can conveniently order your SCHUFA self-disclosure online, so that regular checks are not a big problem.

We recommend applying for the self-disclosure every 3-4 months so that you are always up to date and can quickly take countermeasures in the event of negative entries.

2) Check self-disclosure for false entries

As soon as you receive your self-disclosure, you should check it immediately for false entries.

According to its own statement, SCHUFA has stored more than 800 million data of about 5 million companies and 67 million German citizens.

With this mass of data, mistakes also happen more often, such as confusion of persons and names.

In fact, according to various studies, about one in three SCHUFA reports is incorrect.

Therefore: Check your self-disclosure carefully for incorrect entries and if you discover one, report it to SCHUFA immediately and file a complaint.

3) Check the statute of limitations of the entries.

In addition to simply incorrect entries, there may also be entries in your SCHUFA report that are already time-barred.

If you have not met a payment of less than €2,000 and have therefore received a SCHUFA entry, this entry must be deleted immediately, for example, as soon as you have settled the outstanding debt.

If you have taken out a loan, the information about it remains stored for a further three years after payment of the last installment from the first day of the following year.

Often the banks, financing partners or other creditors forget to report to SCHUFA that the (last) payment has been made.

As a result, your entries are stored for too long and may thus have a negative impact on your SCHUFA score.

Therefore inform yourself about the SCHUFA deletion deadlines and have outdated entries removed by SCHUFA.

This is one of the most effective measures that can improve the improve creditworthiness.

4) Cancel unnecessary accounts and credit cards

If you keep multiple checking accounts and occupy credit cards, SCHUFA evaluates this as an indicator of unreliability.

So, to protect your credit rating, you should cancel all unused checking accounts and credit card contracts.

In addition, you should only switch your checking account in urgent cases, because even frequent account switching has a negative impact on their credit score.

What in turn has a positive effect on your credit rating is if the bank grants you a high overdraft facility or credit line.

You should always choose the highest possible limit, but - very important - never push this limit too far or even overdraw it.

5) Create overview of finances & pay on time

The absolute most important requirement to maintain a high credit score is to have a good overview of your finances and pay bills on time.

Note which outstanding payment claims there are against you, which you have already paid and whether, and if so, how many reminders from which creditors you have received so far.

Meanwhile, there are various apps and websites that make organizing one's finances immensely easier.

This way you always keep track of your payment obligations, which brings us directly to the next point.

6) Pay bills on time

Paying bills is always inconvenient, of course, which is why many people like to avoid it for as long as possible.

However, this has various negative consequences: from reminder fees, to collection proceedings, to a negative SCHUFA entry, from which consequently your SCHUFA score will also suffer.

So always pay your bills on time, because that's the best way to improve your SCHUFA. Tricks and hacks you will then no longer need in any case.

If you receive an unlawful invoice (in your eyes), you should not simply ignore it!

File a written objection to such requests for payment.

How exactly you protect your credit rating in such a case, you can read in our article about the storage period of SCHUFA entries..

7) Seek the conversation with creditors

If you do fall behind on payments, please do not shirk from confronting your creditor.

It may sound banal, but believers are only human. And many people have empathy.

So instead of burying your head in the sand, explain exactly why you've defaulted, when and how you plan to comply with the payment request, and apologize for the late payment.

If you are not (or no longer) financially able to make your payments, you should try to find a solution together with the creditor.

In many cases, it is then possible to agree on a mutually acceptable installment payment or to extend the repayment period.

However, creditors are only gracious if you are open, honest and transparent about the situation.

Additional tip: Make condition inquiries instead of credit inquiries

One mistake that is often made by people looking for a suitable loan is submitting credit inquiries without thinking.

For each credit request, the bank obtains a SCHUFA report on the applicant, either in the form of a credit inquiry or condition inquiry.

Although these two terms seem to be synonyms, there is a significant difference between them:

While a credit inquiry does not directly affect your SCHUFA score negatively, it will be noted on your report for 12 months.

And that can have bad consequences.

An example: You need a loan, make a loan request directly to three banks, but none of them really fits your ideas.

So you apply to another bank.

They can now see that you have previously applied to other banks and may now assume that you have been rejected by all other financial institutions.

This could lead the bank to conclude that you are not trustworthy.

If you would like to compare different loans, you should therefore never make a credit inquiry directly, but first make a condition inquiry.

This is because it is "SCHUFA-neutral" and therefore harmless to your credit rating.

Conclusion

As you could now see, your SCHUFA score has a significant impact on your credit rating.

If your SCHUFA score is bad, all sorts of business relationships can suffer.

Therefore: Always pay your bills on time and regularly check your Order SCHUFA information online, and take direct countermeasures in the event of negative entries.

Then you are also always on the right side!